Grants For First Time Home Buyers In Qld In 2026

Buying your first home is one of life’s biggest milestones - but for many people it has felt increasingly ‘out of reach’. Thankfully, governments at both state and federal level have recognised the challenges of getting on the property ladder. And the good news is that there are several grants for first time home buyers in Qld designed to make that goal more achievable.

From state-based stamp duty concessions to federal government guarantees and savings initiatives, these schemes can help you secure a property sooner and with a smaller deposit.

In this guide, we break down all the first home buyer grants and incentives available in Queensland, including who they’re for, how they work and what eligibility requirements apply. We've also updated this article to include updated provisions made in the Queensland State Budget in June 2026.

The Queensland State Budget in June 2026 updated eligibility rules for the stamp duty concession. For transactions entered into from 1st August 2026, buyers will be required to be Australian citizens, permanent residents or specified foreign retirees to be eligible for this concession.

What Incentives Are Available For First Time Home Buyers In Qld?

There are currently 6 existing schemes that support first home buyers in Qld to get on the property ladder. In addition, the Federal Government’s Help To Buy Scheme launched in 2025 along with the Queensland State Government’s Boost To Buy scheme.

- First Home Owners Grant (Qld Govt)

- First Home Concession (Qld Govt)

- First Home (New Home) Concession (Qld Govt)

- First Home (Vacant Land) Concession (Qld Govt)

- First Home Guarantee – 5% Deposit (Housing Australia)

- First Home Super Saver Scheme (Federal)

- Help to Buy (Housing Australia – coming soon)

- Boost To Buy (Qld Govt)

The other thing to note is that it’s possible to combine a number of these grants and concessions, making it even more beneficial for those buying their first property. Let’s take a look at each one in more detail.

1) First Home Owners Grant - Queensland Govt

The First Home Owners Grant (FHOG) is a tax-free, one-off Queensland Government payment to help eligible first-time buyers buy or build a brand-new home (including substantially renovated/newly built dwellings).

Key Details:

- The maximum $30,000 grant has been extended from 1st July 2026 for four more years.

- It is for brand-new homes only (not established properties).

- Your new home must be valued under $750,000 (including the land) to qualify.

- You must occupy the property as your principal place of residence within 1 year of purchase completion and live there for 6 months.

Why it matters: The FHOG can meaningfully reduce your upfront cash gap when you’re purchasing or building new in Brisbane.

2) First Home Concession - Queensland Govt

The First Home Concession is a Queensland Government stamp duty (transfer duty) discount for eligible first-home buyers purchasing an established house as their principal place of residence.

Unlike the First Home Owner Grant (FHOG), which only applies to new builds, the concession covers established homes - provided you meet the residency and value criteria.

Key Details:

- The value of the property must be under $800,000.

- If the home value is under $700,000, you receive the full concession and pay no stamp duty, which could save you up to $24,525.

- This cannot be used for investment properties.

- You must meet the updated residency and eligibility rules which come into effect on August 1st 2026.

This saving can significantly reduce your upfront costs - potentially worth thousands of dollars in transfer duty savings.

3) First Home (New Home) Concession - Queensland Govt

From 1 May 2025, if you are a first home owner buying a new home or substantially renovated home as your principal residence, you do not have to pay stamp duty.

Key Details:

- There is no value cap on the property.

- Your contract must be signed on or after 1 May 2025.

- Owner-occupier and meet the updated residency and eligibility rules which come into effect on August 1st 2026.

4) First Home (Vacant Land) Concession - Queensland Govt

If you plan to buy land and build your first home on it, the First Home Vacant Land Concession may apply instead.

This concession offers a stamp duty reduction when you purchase vacant residential land with the intention of constructing and living in your first home, if you meet certain requirements.

Key Details:

- Agreements before 1 May 2025: if land is under $500,000, you could save up to $10,675.

- Agreements from 1 May 2025: you might pay no duty on residential vacant land.

- The concession is based on the land value, not the value of the home you build.

- You must build your first home on the land, move in and live there on a daily basis within 2 years of settlement (this time cannot be extended).

It’s an excellent option for those taking a staged approach — purchasing land first and building later.

A key update from the June 2026 Queensland State Budget is that eligibility for all of the above Stamp Duty Concessions will be limited to Australian citizens, permanent residents and specified foreign retirees.

5) First Home Guarantee – 5% Deposit - Australian Govt

The First Home Guarantee (FHBG), run by Housing Australia, allows eligible buyers to purchase a home in Brisbane with just a 5% deposit and no Lenders Mortgage Insurance (LMI). It also supports single parents and legal guardians purchasing with as little as a 2% deposit.

The Federal Government acts as a partial guarantor on the loan, helping first-home buyers overcome one of the biggest hurdles — saving for a large deposit.

Key Details:

- For first-home buyers purchasing new or existing properties.

- From 1st October 2025, there is:

- Unlimited places available

- No income caps

- No waiting list

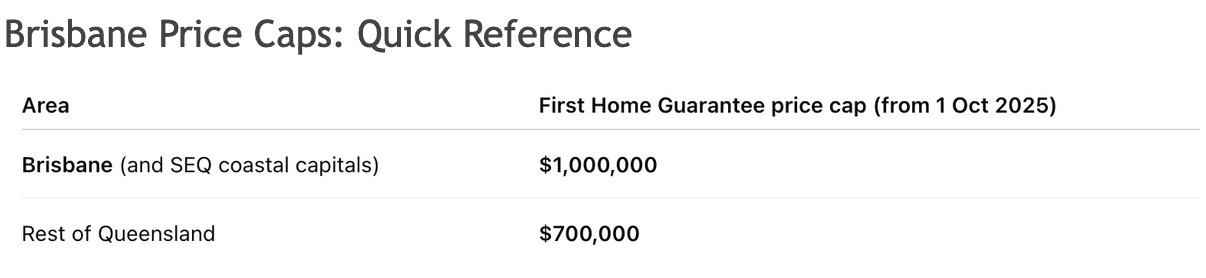

- Increased property price caps: you can use it to purchase a property up to $1 million in Brisbane, the Sunshine Coast and Gold Coast and $700,000 elsewhere in Queensland.

This is one of the most popular federal grants for first-time buyers, as it can save you tens of thousands in LMI costs.

6) First Home Super Saver Scheme - Australian Govt

The First Home Super Saver Scheme (FHSSS) allows first-time buyers to save for a home deposit inside their superannuation fund.

You can make voluntary contributions (before or after tax) to your super and later withdraw them — plus any earnings — to help with your deposit.

Key Details:

- Up to $15,000 in voluntary contributions can be released per financial year, capped at $50,000 in total.

- You must apply to the Australian Taxation Office (ATO) to release funds.

- Only voluntary contributions (not employer contributions) count towards the scheme.

- It’s a tax-effective way to grow your deposit faster.

This scheme can offer a more disciplined and tax-efficient savings path to home ownership.

7) Help to Buy Scheme (Launching Soon) - Australian Govt

The Help to Buy Scheme is a shared-equity program expected to launch soon under the Australian Government.

It allows eligible buyers to co-purchase a property with the government, which contributes a portion of the purchase price (up to 30% for existing homes and 40% for new homes).

In return, the government retains an equivalent equity share in the property.

Key Details (expected):

- Smaller deposit required and reduced loan amount.

- Income and property price caps will apply.

- You must live in the property as your principal residence.

- 10,000 places available per year.

- Available to both first-home buyers and those returning to home ownership.

This initiative is designed to help more Australians enter the housing market and reduce ongoing mortgage costs.

8) Boost To Buy Scheme - Queensland Govt

The Boost To Buy home ownership scheme was announced by the Queensland State Government as part of the 2025-26 state budget. Similar to the federal government scheme it will provide an equity contribution to eligible Queenslanders who are saving for their first home.

Key Details (expected):

- Boost to Buy will offer an equity contribution of:

- Up to 30% for new homes

- Up to 25% for existing homes.

- Minimum 2% deposit will be required

- Property price cap of $1 million

How Sapphire Finance helps Brisbane first home buyers

A specialist mortgage broker like Sapphire Finance can save you time, stress and money by:

- Confirming eligibility across concessions and federal schemes.

- Comparing lenders that offer the First Home Guarantee and competitive rates for first home buyers.

- Structuring your loan to align with deposit size, cash flow and long-term goals.

- Co-ordinating paperwork so your concession or scheme is applied correctly at the right stage.

- Advising on strategy to minimise LMI and stamp duty, and to use FHSSS effectively.

- Local guidance on Brisbane prices, caps, and bank policies to improve approval confidence.

Getting started: your action plan

- Check eligibility for the relevant Queensland concession and federal schemes.

- Estimate your deposit and consider whether FHSSS could improve your savings position.

- Assess property price caps for your target area.

- Speak to Sapphire Finance to map the best pathway and secure pre-approval with the right lender.

FAQs: Grants for First Time Home Buyers in Qld

What grants are available for first home buyers in Queensland?

Eligible buyers may access:

- First Home Owners Grant (Qld Govt)

- First Home Concession (Qld Govt)

- First Home (New Home) Concession (Qld Govt)

- First Home (Vacant Land) Concession (Qld Govt)

- First Home Guarantee – 5% Deposit (Aus Govt)

- First Home Super Saver Scheme (Aus Govt)

- Help to Buy (Aus Govt – coming soon)

- Boost To Buy (Qld Govt - coming soon)

Can I use more than one grant or concession?

Yes, in some cases you may combine a number of grants, concessions and incentives — provided you meet all eligibility criteria.

Is the $30,000 First Home Owners Grant still available in Queensland?

Yes, the maximum grant of $30,000 has been extended until June 2026, after which it will revert to $15,000.

Do these grants apply to investment properties?

No. All first-home buyer grants and concessions are for owner-occupied properties only.

How can a broker help with first-home buyer grants?

A mortgage broker such as Sapphire Finance can help confirm your eligibility, prepare your loan application, and coordinate with participating lenders to access the relevant scheme.

Do I need to repay stamp duty concessions?

No. Concessions reduce the duty you pay upfront but you must meet occupancy and eligibility rules to retain them.

Do I repay Help to Buy equity?

Help to Buy is shared-equity, so the Government’s share is repaid when you sell, refinance, or through agreed voluntary repayments.

Can I use FHSSS and a federal guarantee together?

Yes. FHSSS helps you build a deposit, and the guarantee can reduce the deposit needed and remove LMI, subject to lender and scheme rules.

Does the First Home Guarantee still have limits?

From 1 October 2025 there are no place limits and no income cap. Property price caps in Queensland are $1,000,000 for SEQ metro (Brisbane, Sunshine Coast, Gold Coast) and $700,000 elsewhere.

Final Thoughts

For first-home buyers in Queensland, understanding the range of grants, concessions, and guarantees available can make a huge difference to your buying power.

From state stamp duty concessions to federal deposit schemes, there are multiple paths to home ownership depending on your circumstances.

At Sapphire Finance Brokerage, we help first-home buyers navigate the complex world of grants, incentives and concessions and secure competitive loans that align with your financial goals.

If you’re exploring your options or want to confirm your eligibility for any of these first-time buyer grants in Qld, our First Home Buyers Mortgage Broker is here to help.

All the information contained in this article is correct at the time of writing (October 2025) but is subject to change. The information contained in this post is for general guidance only and does not constitute personal advice.

.jpg)

Mortgages for the Self Employed: How Do Loan Options Differ for Self Employed Borrowers?

Types of Home Loan: What Mortgage and Home Loan Options Are Available In Australia?

.svg)